Venture Capital's Fourth Turning

In 1997, the two men who coined the term “Millennial” wrote a book called The Fourth Turning. In it, they took the phrase “history doesn’t repeat, but it rhymes,” and added a structural framework to that idea.

Their framework said that every ~80-100 years (the length of a long human life) you had a series of four “saeculums,” or turnings, each lasting about 20 years. They framed the latter half of the 20th century and onward with this framework:

- (1) The High (1946-1964): Strong institutions, weak individualism, confident collective optimism.

- (2) The Awakening (1964-1984): Spiritual and cultural upheaval; the civic order gets attacked in the name of a new values regime (e.g. the Sixties counterculture).

- (3) The Unvraveling (1984-2008): Strengthening individualism, weakening institutions, declining trust, cynicism (e.g. the culture wars)

- (4) The Crisis: a decisive, often violent reckoning where the old civic world order is torn down and replaced. The American Revolution, the Civil War, the Depression + WWII. Writing in 1997, they predicted the next Crisis would ignite around 2005-2008 and climax in the late 2020s.

Between 9/11 and the Financial Crisis, I’d say they nailed the Crisis ignition, and the 2020s are certainly feeling like a climax. Kinda spooky, right? Feels like a book worth revisiting.

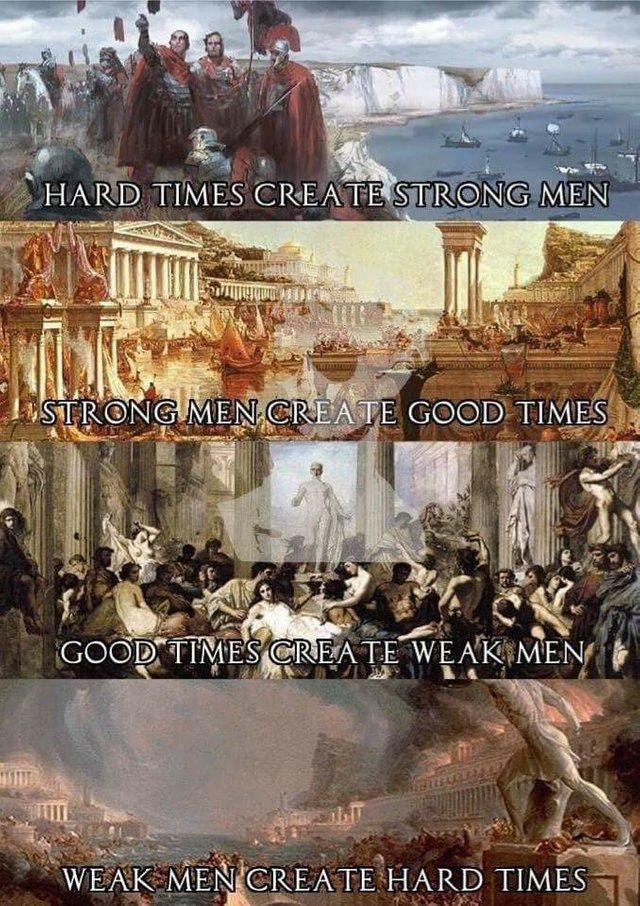

In a similar vein, there is a meme using images like Thomas Cole’s “Course of Empire“ series to reflect the phrase, “hard times make strong men, strong men make good times, good times make weak men, weak men make hard times.”

An exceptional, and comparable, line exists in Herdotus’ Histories when Cyrus says, “Soft lands breed soft men; wondrous fruits of the earth and valiant warriors do not grow from the same soil.”

I believe that venture capital is experiencing a comparable Fourth Turning. Venture was born out of the crisis of WWII with an industrial surge and no system to build it; the government bootstrapped a capability with the help of Bell Labs, ARDC, etc., but needed something more sustainable going into the Cold War.

- (1) The High (1960-1980): The new civic order of venture capital emerges. Davis & Rock in 1961, Sequoia and Kleiner in 1972. A confident, cohesive professional craft forms; apprenticeship, power law discipline, partnership norms, strong institutions, shared values, collective confidence.

- (2) The Awakening (1980-2000): Venture catches religion as values are upheaved from a quiet financial craft to a world-changing mission. From Doerr-era mission-driven evangelism to the rapid succession of PC and internet rattling the world. Disciplined guild ethos of the 1970s overheats in the Dot Com amidst a genuine spiritual upheaval.

- (3) The Unraveling (2000-2020): Mission-driven and founder-friendlies win the culture war and become dominant, dismantling centralized standards. a16z starts in 2009 and shatters the partnership model with the platform model while YC industrializes seed investing. The single cohesive guild culture splinters into a thousand different brands, strategies, and personalities. Strengthening individualism (e.g. solo GPs), weakening shared norms (bad behavior abounds).

- (4) The Crisis (2020-2040?): That fragmented, individualized orders gets torn down. COVID may have been the spark, but the 2022 rate shock exacerbates it, we see SVB collapse, plus the 2021 vintage overhang from Tiger, SoftBank et al. Choking denominator effect, zombie funds, capital concentration. Every rebirth is catalyzed as the Crisis forges the new world order. Ours? The AI Supercycle. Do companies need more capital or less? Is capital a barbell or a spectrum?

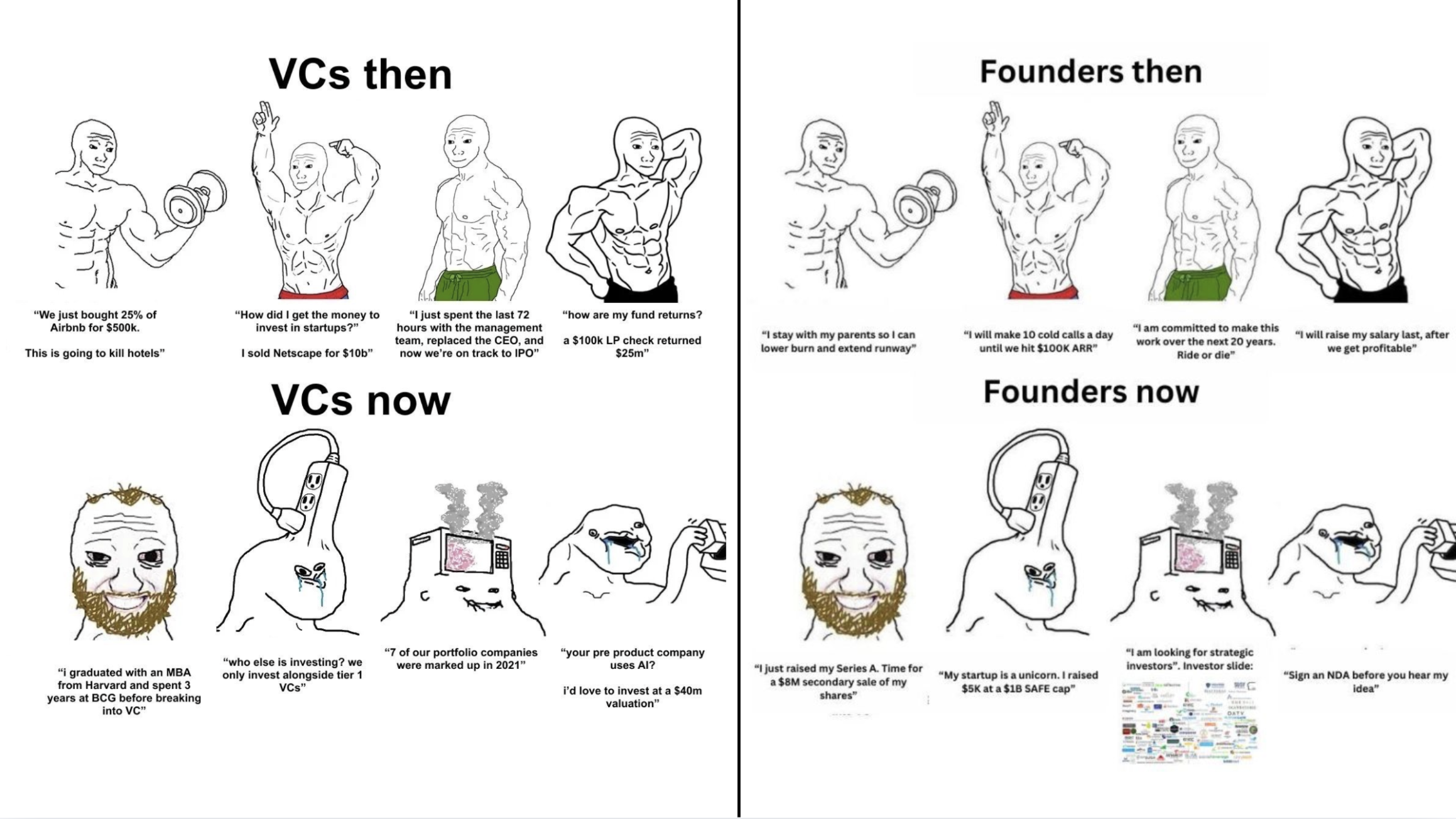

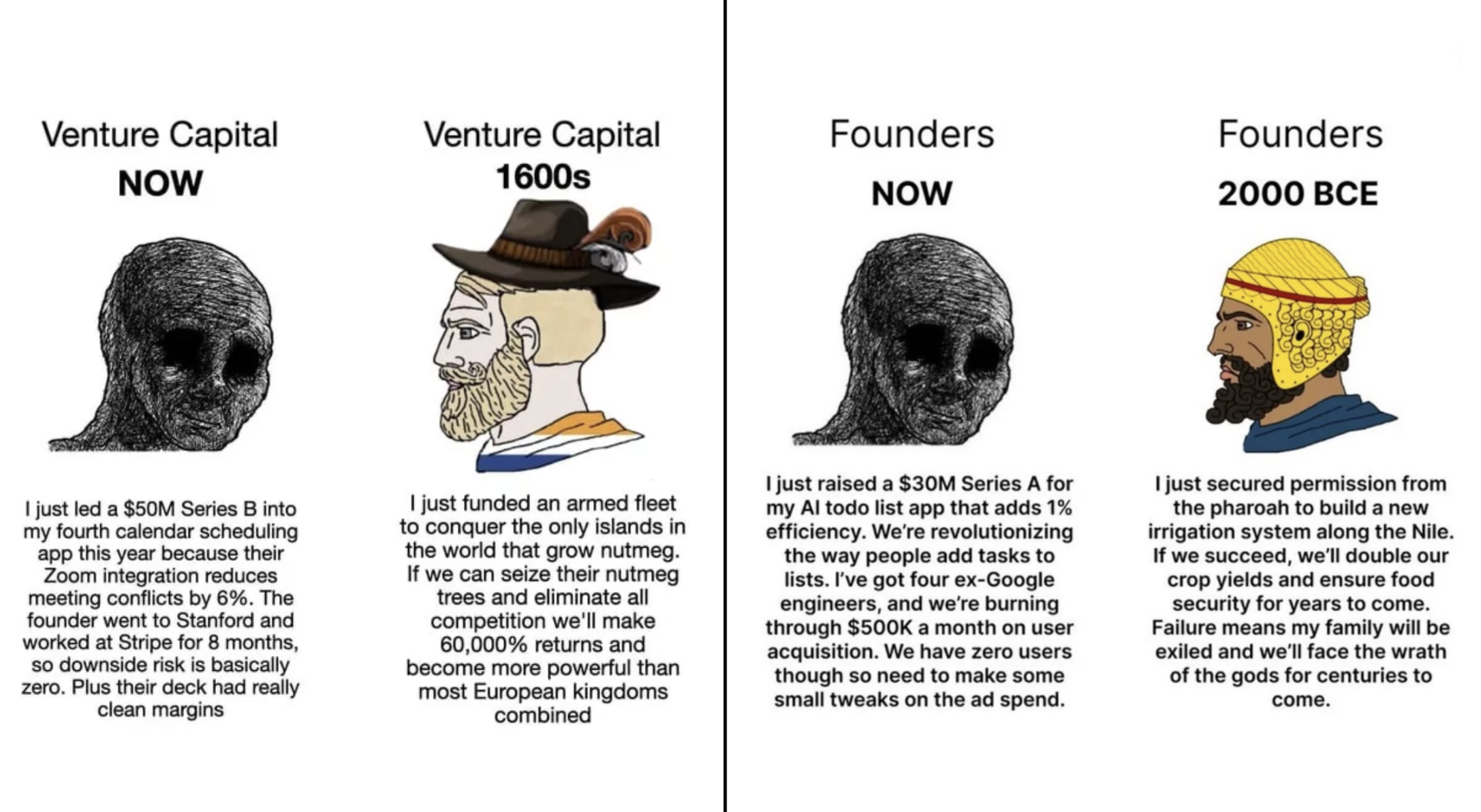

What’s more, we’ve already started to see the emergence of our meme class representing the “course of empire” for venture capitalists and founders.

There’s an inherent sarcastic appreciation for what was and what is and the reality that something has been lost.

Where we look at the “strong men” that built the foundational technological empire upon which so much of life has improved we note a clear difference between what has gone before and what we have today. So what will venture capital’s Fourth Turning consist of? And what will come out the other end of that Crisis?

Characteristics of Crisis

Each day we see the cracks expand in the default funding mechanism of technological progress.

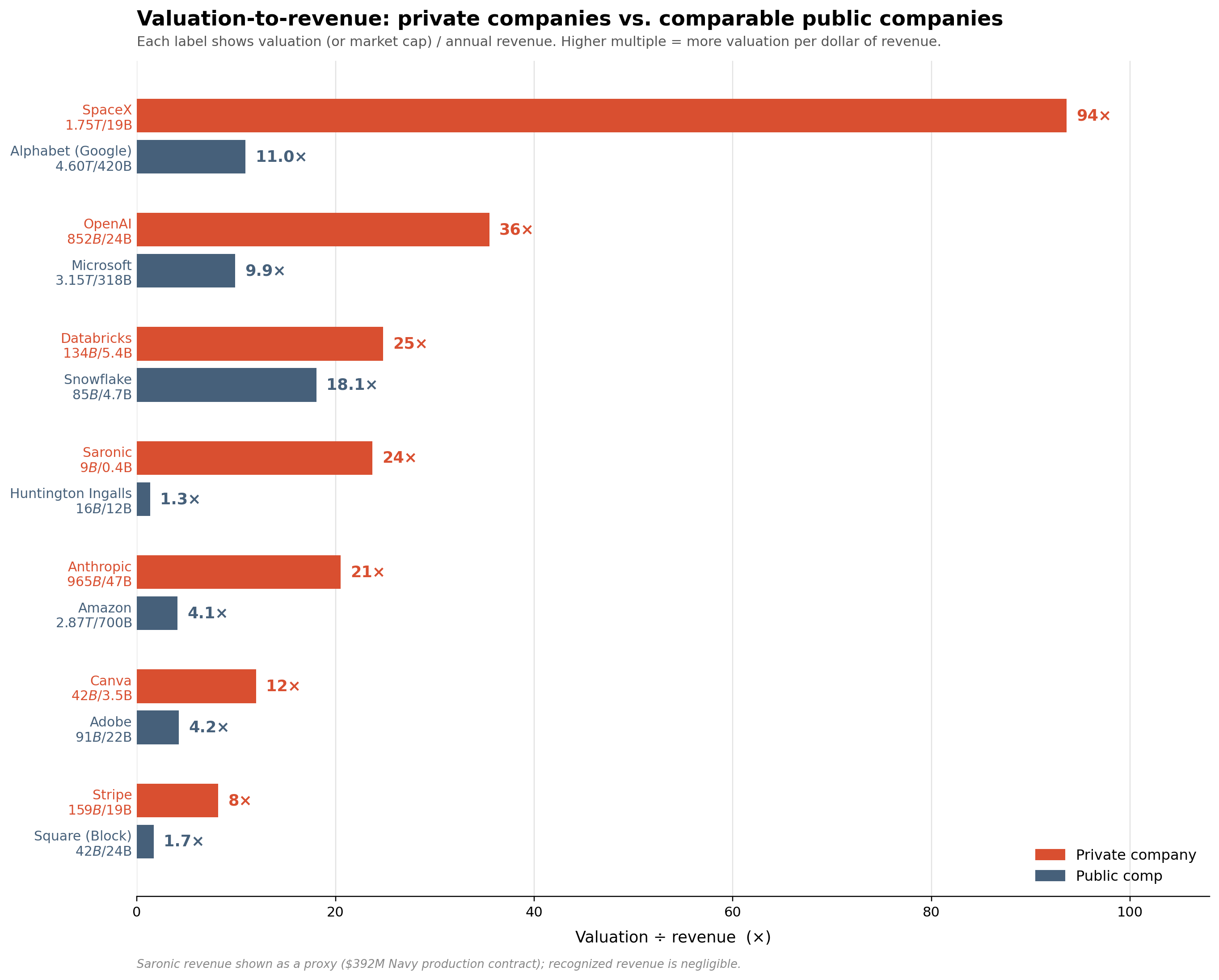

Valueless Valuations

One of the clearest post-excess hangovers is valuation. Startups have no fundamental correlation to their valuations. The age of excess has established a modicum of mental rot where valuation is a clearing price, with no bearing on a summation of economic value creation potential.

I got into a debate with another VC once about whether the total volume of VC-backed outcomes has increased and he pointed to dozens of companies valued at $10B+. But the reality is that those marks effectively don’t mean anything. There’s $3.2 TRILLION in unrealized value locked in the private markets. If those materialize, then venture as an asset class could mean a lot more. But, increasingly, it feels much harder to realize the high-priced ambitions that VCs have made a fundamental part of their model.

In the mean time, the lack of material outcomes are breaking the broad model of venture. Because exits won’t come, the fund structure* itself* is being torn down and rebuilt with financial engineering: continuation vehicles, NAV loans, tender offers, GP-led secondaries. As a result, 72% of LPs are reporting reducing their VC allocations.

Some are pure hype; pre-revenue labs being valued at multi-billion dollar valuations. Others represent dislocations from public markets. The obstacle is the uncertainty around what most of these companies will be worth in the long-run. But people are looking at dozens of examples like the below and scratching their heads:

But the obvious pushback on the eve of SpaceX’s long-awaited IPO is that the outsized outcomes are coming! People will say OpenAI, Anthropic, and even SpaceX are the new hyperscalers. But are they? Or are they tentative hype-cycle benefactors with deep question marks around their long-term viability?

The default optimism is to say things like SpaceX is undervalued at $1.75T, its launch business is immaterial relative to the $23T of TAM it’s going after, and the $26B of annual revenue its receiving from folks like Anthropic and Google is definitely durable and not incidental.

And the default logic to support this kind of disparity is the promise of future opportunity. That’s not to say that these exceptional companies won’t prove to be relatively cheap today in the future as their businesses continue to swell. Many have done just that. But, despite the reality of the upside of the power law, that 80/20 split also means that 80% of the companies will NOT drive comparable outsized value to the 20% of outliers that will. As a result, the majority of private companies are likely overvalued and always will be.

AUM-Measuring Contest

The world of venture capital juxtaposed against those valuations begs the questions; why do all these companies need to be so much bigger than ever before? Because the bigger the funds, the bigger the outcomes need to be.

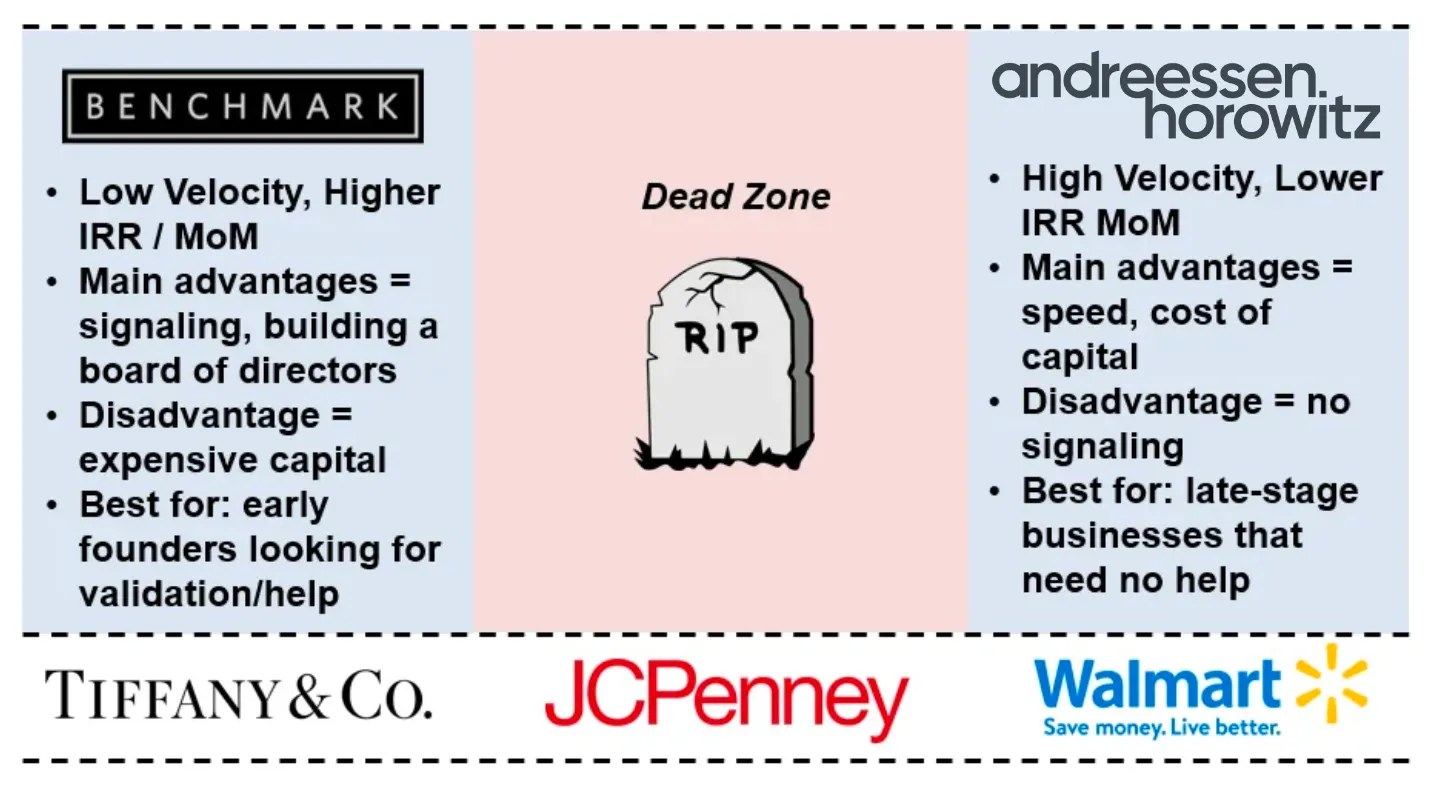

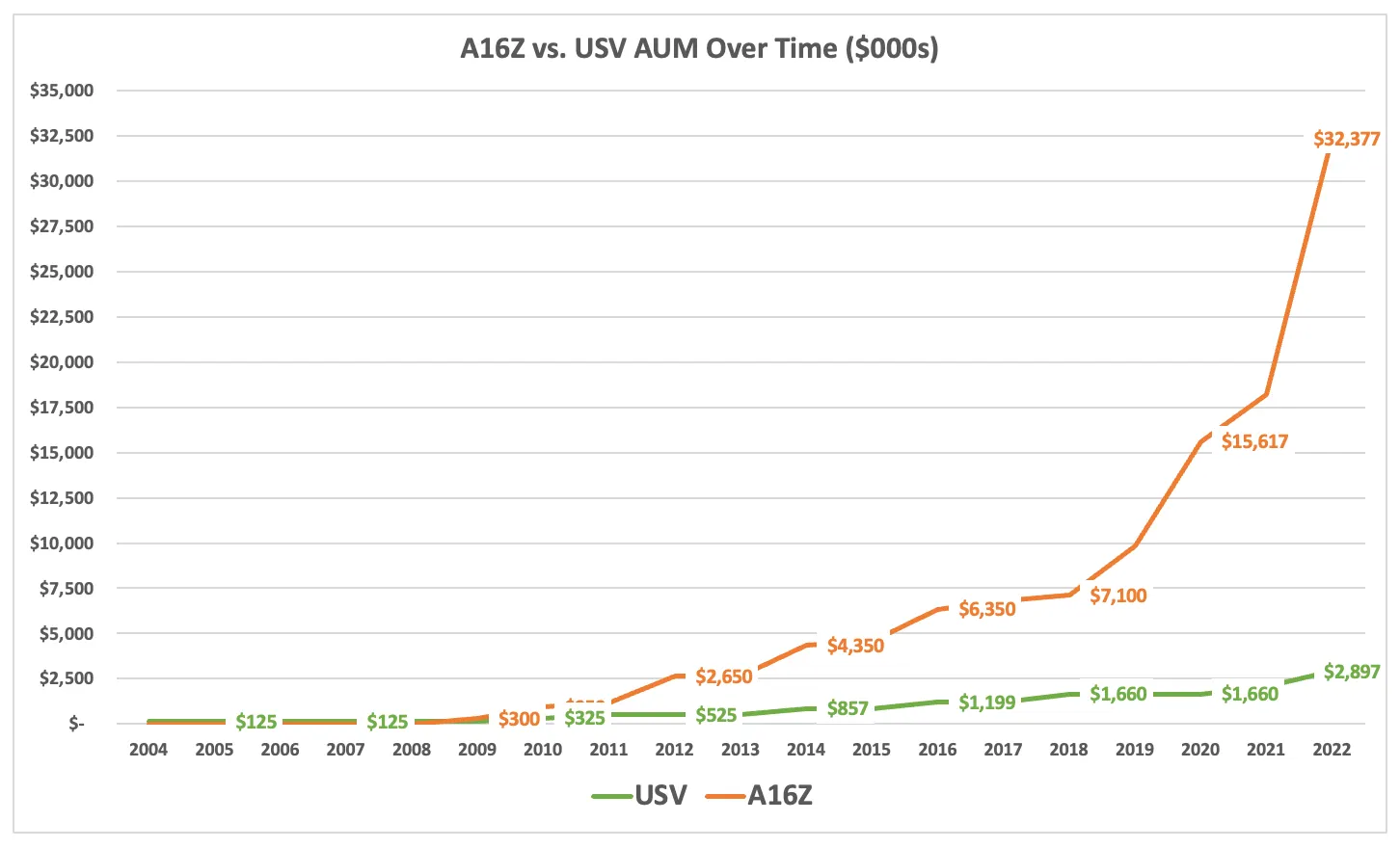

What gets measured gets managed and the focus is, increasingly, being placed on fund size. There has, historically, been a bifurcation between fund sizes. My most popular pieces I’ve ever written was The Puritans of Venture Capital where this was the whole point. “Puritan cottage keepers” on the one end and “capital agglomerators” on the other.

Firms like USV, Benchmark, etc. were built around a disciplined mentality of “your fund size is your strategy.” Meanwhile, capital agglomerators, like a16z, Lightspeed, etc. raced to build larger and larger empires, fueled by multi-billion dollar pools of AUM.

This bifurcation has been eroding for years, but it may have lost its most staunch champion. This past week, Benchmark announced it had raised $2B in new funds. The Cottage Keepers of yesteryear are more akin to Unicorns in rarity than the run-of-the-mill “$1B+ valuation.”

The logic behind Benchmark’s increased fundraise is an acknowledgement of the changing landscape. Bigger companies raise bigger rounds with bigger expectations. And if you’re going to compete, you have to have the capital to play along.

In The Puritans of Venture Capital, I made the point that the last time Benchmark considered raising more capital was in 2021 when they lost out on investing in Clubhouse against a16z. Prior to that, the last Benchmark actually raised a bigger fund was in 1999.

Is this history repeating itself? Rhyming? Or something fundamentally new?

The issue is whether the game, in the long-run, is actually changing. It most certainly is in the short term. AI companies absorbed 81% of all US venture capital in Q1 2026, up from 55% a year earlier. That massive capital influx has pushed folks like Benchmark out from participating; they didn’t invest in OpenAI, Anthropic, or any of the other foundation model companies.

But at some point we have to stop and ask… are those rounds even venture capital anymore? (Side note: Will Quist says “no.”)

The largest are actually more like sovereign / strategic investments: OpenAI’s $122B raise was the largest private round in history at an $852B valuation, and sovereign funds like GIC, Temasek, QIA, and Mubadala have become the definitive players, treating frontier AI as a sovereign-wealth-class asset rather than venture. Akin to new-age oil money.

What’s more, the entire ecosystem is built around dramatically complex and interconnected circular incentives / funding mechanisms. Nvidia committing up to $100B to OpenAI to build data-centers, Google raising $80B in equity because bank financing is choking on the $1T+ investment this whole ecosystem is requiring.

All of it is starting to “rhyme” with the vibes from 1929 or 2000; the kind of economic intertwining that typically precedes a Crisis climax rather than its opening.

Not Pretending Anymore

Even more so than the shifting economic model of venture is the cultural ethos.

In the early 2000s, Google established the motto, “Don’t be evil.” Facebook’s motto of “move fast and break things” was never meant to extend to breaking democracy or people’s brains. OpenAI was started in 2015 as a non-profit to benefit all of humanity until they realized that benefit was so dramatically more monetizable than they originally realized.

Technology, for a long time, had a “make the world a better place” energy. So much so that it was a fundamental part of the joke in a 2014 episode of Silicon Valley making fun of a series of TechCrunch Disrupt pitches.

You look at the categories that used to be hot and how they were framed, and it feels like a relic of a different civilization.

MOOCs (”education for everyone”), One Laptop Per Child, Google Fiber, Facebook’s Internet.org/Free Basics (”connect the next billion”) the “sharing economy” sold as community (Airbnb “Belong Anywhere,” Uber “transportation for everyone”).

Now, everything feels like it’s about arbitrage. Labor arbitrage in marketplaces, the gamblification of everything with prediction markets, AI companions optimized for time-on-app, content farms producing the purest of slop.

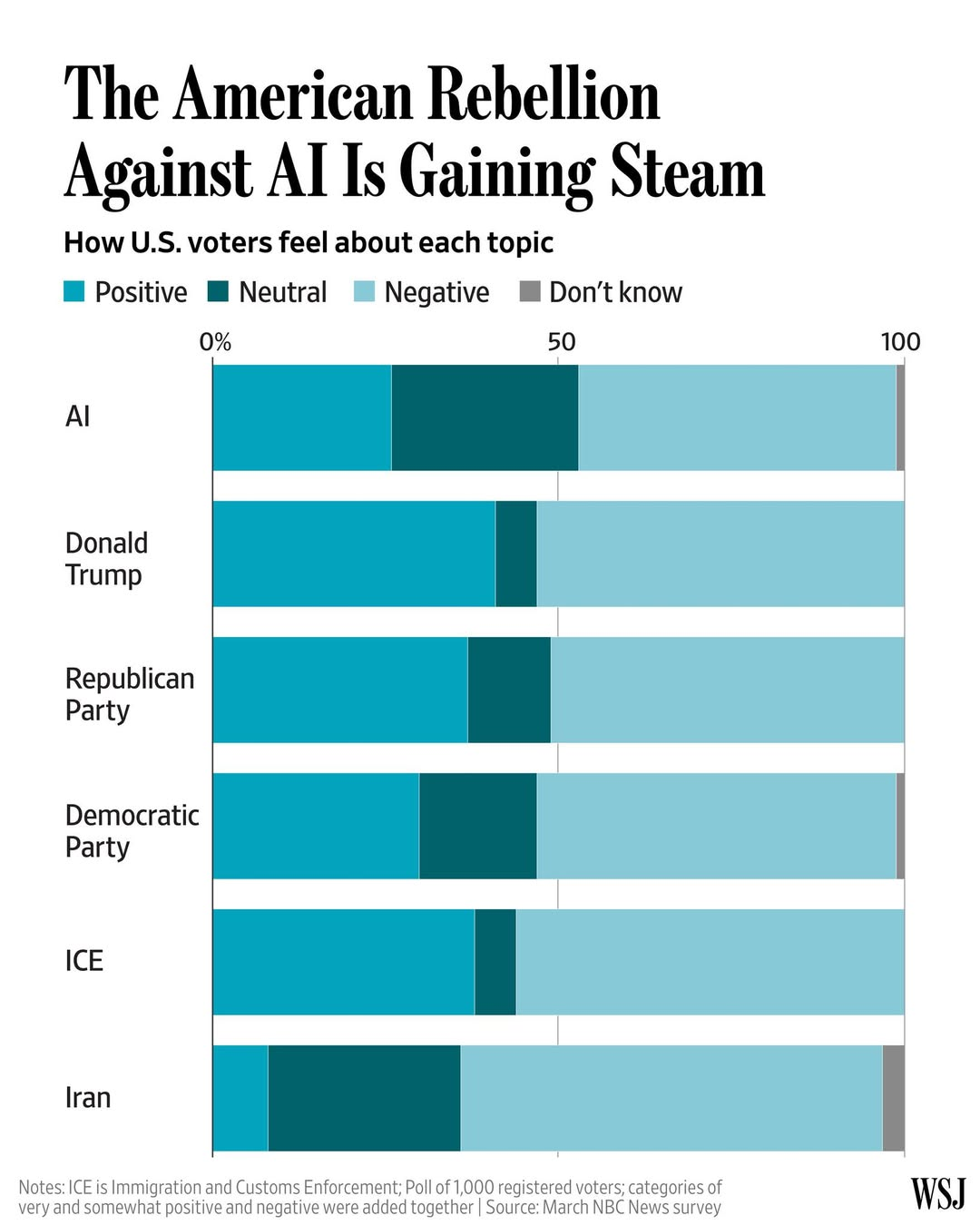

That moral repositioning isn’t new; it’s been playing out for the last several years. But now its coming home to roost. People have a default negativity when it comes to technology.

71% of Americans would oppose a data center near their home, up from 42% nine months earlier. A record number of data centers were canceled in Q1 2026 amid community resistance, and Morgan Stanley flagged public pushback as a binding constraint on AI buildout. Data-center even recently opposition helped tip recent elections in Virginia and Republican-leaning Georgia; candidates in both parties now treat it as toxic.

In fact, AI overall is viewed less favorably than Donald Trump or ICE.

The prevalence of gambling apps, read: prediction markets, has also become a flagship venture category, with companies like Kalshi reaching $22B valuation. Beyond just having a corrosive impact on young people getting addicted to gambling under the guise of intellectual arbitrage, it also plays right into power manipulation. Predictions markets are easy wins for insider trading and politicians or campaign staffers to treat inside information like a tradable asset.

All of that, combined with VCs’ broader moves into explicit political activity, venture is transitioning from financier to governing-class actor. That’s a fundamental signal marker for the Fourth Turning that Strauss and Howe articulated in the book.

For its whole history, venture operated inside the civic order’s economic subsystems. A financier allocates capital under rules that someone else writes. But a governing-class actor is something categorically different: instead of following the rules, it writes new rules, staffs its own institutions, and provides its own definition of “legitimacy.”

The Unraveling of the first two decades of the 21st century broke the old system. You see it in the dissolution of institutional trust across the board. A stark contrast between the old-guard “values” that were trying to align with existing systems and “make the world a better place” vs. the new-age stance is Marc Andreessen’s Techno-Optimist Manifesto. You would certainly expect it to lay out the case; what is the clarion call for techno-optimists everywhere? But what it also does is explicitly articulates “the enemy.”

“Our present society has been subjected to a mass demoralization campaign for six decades – against technology and against life – under varying names like “existential risk”, “sustainability”, “ESG”, “Sustainable Development Goals”, “social responsibility”, “stakeholder capitalism”, “Precautionary Principle”, “trust and safety”, “tech ethics”, “risk management”, “de-growth”, “the limits of growth”.”

Almost every facet of technology’s new shape is a representative seizing of the “old guard.” VCs moving directly into government roles, crypto and stablecoin enable a push into monetary control, defense-tech and American Dynamism reaches for the state’s monopoly on organized violence, tech-enabled super-PACs operating as open kingmakers, not quiet donors, network-state and “exit” ideas, charter cities, the Balaji-style ambition to literally reincarnate new nation states.

We’re not making the world a better place. We’re reshaping the world in our image.

Funding “What Matters”

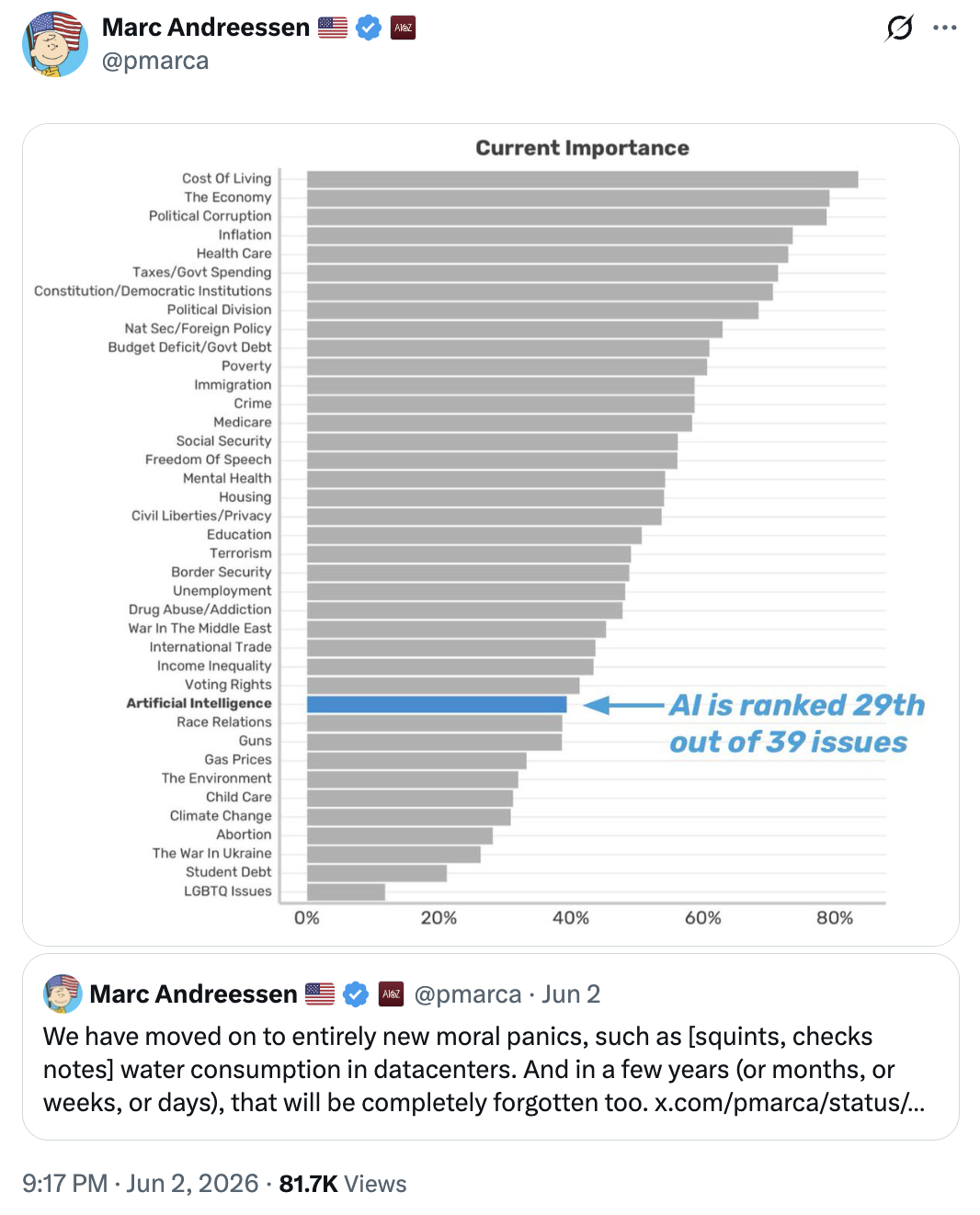

Recently, Marc Andreessen posted about the new moral panic of water consumption in data centers and made the argument that its just the latest entry in a series of “moral panics” that will go away because they’re not actual issues.

And I agree. A huge swath of the anti-data center movement feels manufactured or deliberately misconstrued, whether through Chinese foreign actors or honest-to-goodness stupid mistakes, like Karen Hao doing bad math in Empire of AI.

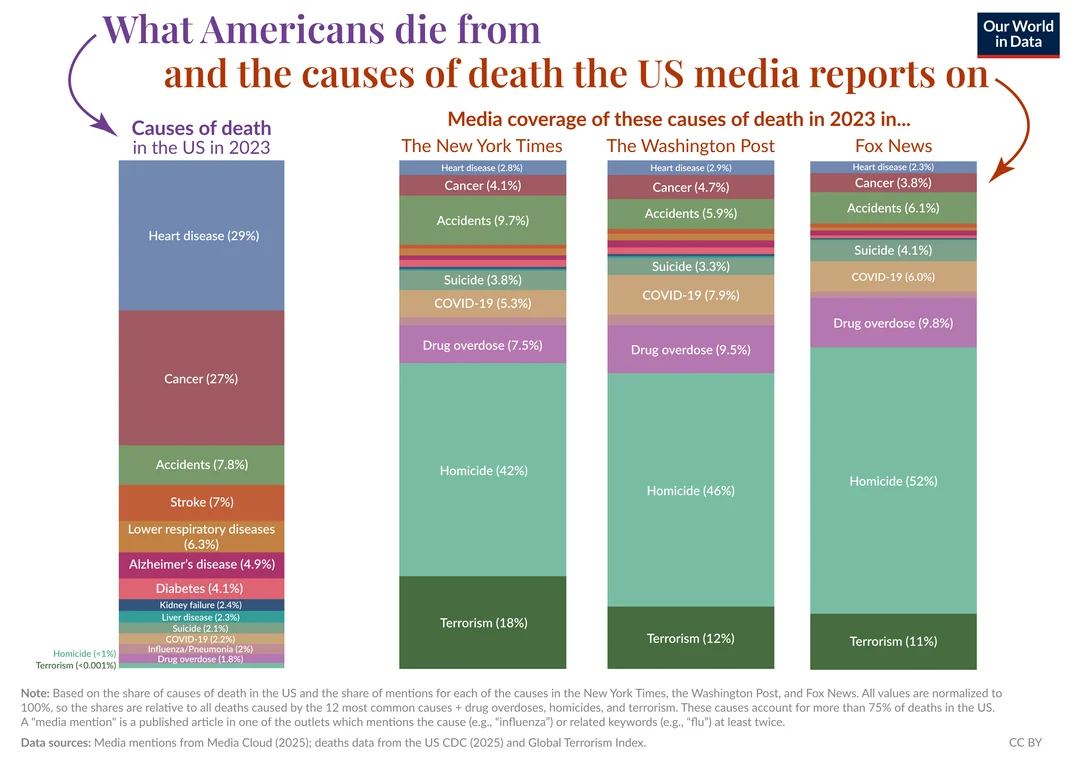

But this chart also reminds me of a similar chart that compares what Americans actually die from to how much its covered in the media.

Despite over 50% of deaths being caused by heart disease and cancer, they represent ~7% of media coverage. Instead, the media spends almost 60% of its coverage on homicide and terrorism, despite that leading to less than 1% of American deaths.

That feels fundamentally yucky, doesn’t it?

There’s a mixed bag here in terms of what it means for venture capital. On the one hand, I would say that we can make the point that AI is low on people’s list of issues. But then also acknowledge its eating 80%+ of the capital in any given quarter. So are we solving real problems?

The next answer is, “well, AI will have an impact on all sorts of categories.” And that’s certainly true. But the saddest part is that we don’t particularly care about funding solutions in those categories. We care about TAM expansion. We invest money into problem areas, not because they represent problems worth solving, but because they represent sizable financial windfalls.

I gave an interview a few weeks ago where I pushed back on this approach:

“Everybody should be having more philosophical debates about the things that they are investing in. We don’t have nearly enough philosophical debates about the implications. We just say, ‘Hey, this is a hot technology and it looks like it’s ripping and people really like it’ and it’s just so blinders on, focused on ‘big market. Let’s do it.’ I think more people should have to embrace the the philosophical stick that they’re picking up because there’s consequences at the other end of that stick.”

Just one example. We have a portfolio company that went from $24M to $50M in high-margin revenue in Q1 of this year alone and is on track to end the year at $100M. The founder is exceptional, they have massive enterprise relationships with some of the biggest insurance companies in the world, and they’re solving a fundamental problem that can improve the lives of the sickest people in the country.

I introduced them to a few large “Tier 1 VCs” for conversations around their most recent fundraising round. Many of them engaged with the company, but one of them said to me, “I just don’t think this is really differentiated.” I genuinely almost laughed in their face, given the fact that they just finished investing in their fourth AI foundation model company and their third AI model orchestration company.

The Phoenix Reborn

So… what happens now?

Criticizing anything can be a real struggle because everything has nuance.

Has technology become riddled with arbitrage-driven exploitation? Yes. But has it also always had a role in improving people’s quality of life? Also yes.

And that continues. Biotech, GLP-1s, industrialization, etc.

Focusing on The Fourth Turning can feel like a Nihilistic exercise; it ends with the Crisis. Bummer. But the reality is the Crisis is the only turning that builds. The High doesn’t author its own values; it inherits them from the Crisis that came right before it. The confident, institution-rich America of 1946 wasn’t conjured in 1946. It was forged between 1929 and 1945. The worldview of the rebirth gets written during the reckoning, not after it.

So the Crisis isn’t the point to languish on. The focus, instead, should be on the rebirth. The Rising. The Unraveling hollowed out the old order. But, candidly, there’s a lot that needed to be hollowed out. The world is too complex and moving too fast to forever be determined by old white dudes in suits doling out cash. The evolution within venture capital is good. You’ve got to break a few eggs!

As painful and demoralizing as the Crisis can be, it is effectively opening up the room where someone decides what replaces it. And right now, that someone is us. Every check written and every fund raised is a vote on what the next forty years will value. As I’ve written about before, investments are a leading indicator of your beliefs, and the industry is voting, whether it’s thinking about it or not.

So, as much as we can chronicle the rot left over from the era of excess, we also have to acknowledge the critical reality that will shape the new world order.

AI is not bad. The same model architecture that powers the slop farm also powers my portfolio company going from $24M to $100M while helping the sickest people in the country. GLP-1s are quietly rewriting the metabolic future of tens of millions of people. Foundation models are folding proteins, reading scans, and compressing discovery timelines that used to be measured in decades. Fire is the oldest dual-use tool we have. It cooks a meal AND it burns down a house, and the difference has never been the fire’s decision. It’s ours.

Industrialization is not regression, either. Granted, I’ve spent a lot of this year nervous about venture’s lurch toward raw political power. But. Re-learning how to build ships, munitions, energy, and chips is not the same thing as a power grab. It’s the thing that keeps free societies defensible in a world where the alternative is very much knocking on our door. A liberal democracy that has forgotten how to make things is a liberal democracy with an expiration date. Rebuilding that capability is among the most genuinely good things this Crisis could produce.

Who Are We?

So… are we in a Crisis?

Yes. Unambiguously. Negative favorability, data-center revolts, SVB’s collapse, the $3.2 trillion of trapped value, the moral hangover… welcome to the Fourth Turning.

Strauss and Howe’s book doesn’t leave it at “here it comes!” The question, instead, is who you’ll be inside the Crisis?

Hard times make strong men. But that’s not the whole story. Because nothing makes you strong by default. Plenty of hard times have produced bitter, brittle, smaller people; the cycle only rhymes when somebody chooses to make it rhyme. A Crisis is a refiner’s fire, and fire does two very different things to two different metals. It tempers the steel that was worth tempering. But it consumes everything else. What you walk out as depends entirely on what you carried in.

The Hero generation that Strauss and Howe say comes of age in every Fourth Turning isn’t born heroic. It becomes heroic by being handed an impossible decade and choosing to: (1) build instead of extract, (2) steward instead of strip-mine, (3) fund the thing worth solving instead of the thing with the biggest market. That’s the menu of options.

So, so, SO many people are overcome with pessimism. It is SO much easier to be negative and grumpy and defeatist. Cynicism is free. And, increasingly, its in-group reinforcing. You belong by being negative. The other side of the coin isn’t as simple. Hope requires something of you. Maybe in the olden days, you could smile and assume the world around you would get better without you contributing anything. But that is not the times we live in. If you want to be optimistic, you have to put something on the altar. You have to strive for it. But as for me and my house, we choose optimism. Because the alternative is to concede the rebirth to the people writing the slop.

So… what kind of men and women will we be coming out of this?

Let’s be the kind of people that build the next High worth living in.

God speed.